Cosigning can help your student succeed

Competitive Undergraduate Rates:

Fixed rates: 2.89% - 17.49% APRfootnote 1

Variable rates: 3.75% - 16.37% APRfootnote 1

Lowest rates shown include the auto debit discount. Only the most creditworthy applicants who choose the interest repayment option may receive the lowest rate.

1. Tell us some basics

2. Invite your student

3. Sign and accept

You’re there for your student

Many students don’t have the credit history to take out a loan on their own. With a creditworthy cosigner, your student may have a better chance to be approved and may get a lower interest rate. A cosigner can be a parent, or any creditworthy adult who, like the borrower, will be fully responsible for making on-time payments on the loan.

footnote 2

You both can feel confident about cosigning

From tuition to living expenses, 100% of all your student’s school-certified costs can be coveredfootnote 3

Your student can apply to remove you from the loan after graduation, making 12 on-time payments, and meeting other requirements.footnote 4

Families saved over $345 million compared to PLUS origination fees over the last 10 years.footnote 5

If you choose to make payments while your student is in school, the total cost of your loan may be lower.footnote 1

Compare interest rate types

You have options. See whether fixed or variable rates might be best for you and your student.

Fixed means your interest rate never changes.

2.89%

to 17.49% APRfootnote 1

If you want a predictable monthly payment, this is the way to go.

Variable interest rates go up or down as the market changes.

3.75%

to 16.37% APRfootnote 1

This means your monthly payments may also change—they might be higher if interest rates rise and lower if they fall.

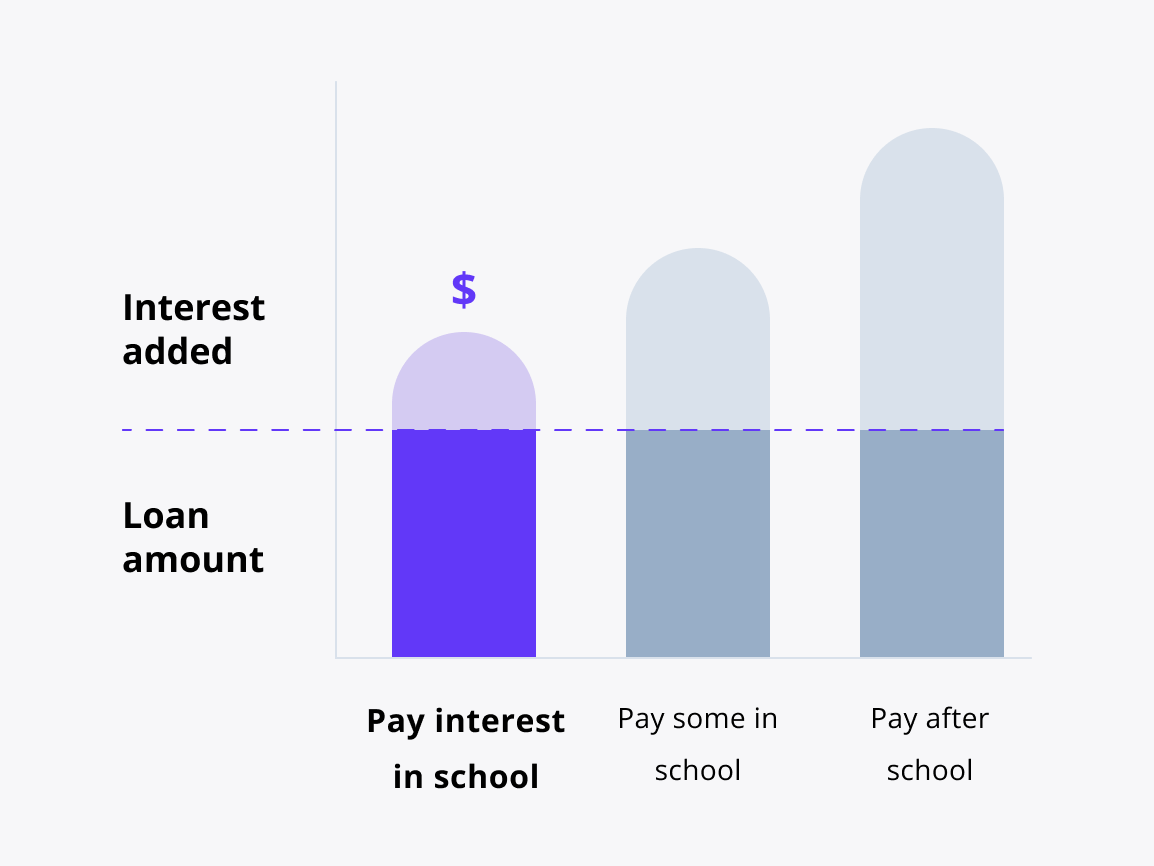

Interest repayment option

How does it work?

You pay your interest every month your student is in school and in grace (the 6 months after).footnote 1

This is a great option if you want to save the most.

Freshman students may save 17% on their total loan cost by choosing interest repayment instead of deferred repayment.footnote 6

Keep in mind:

You might have higher monthly payments, but the total cost of your loan may be lower.

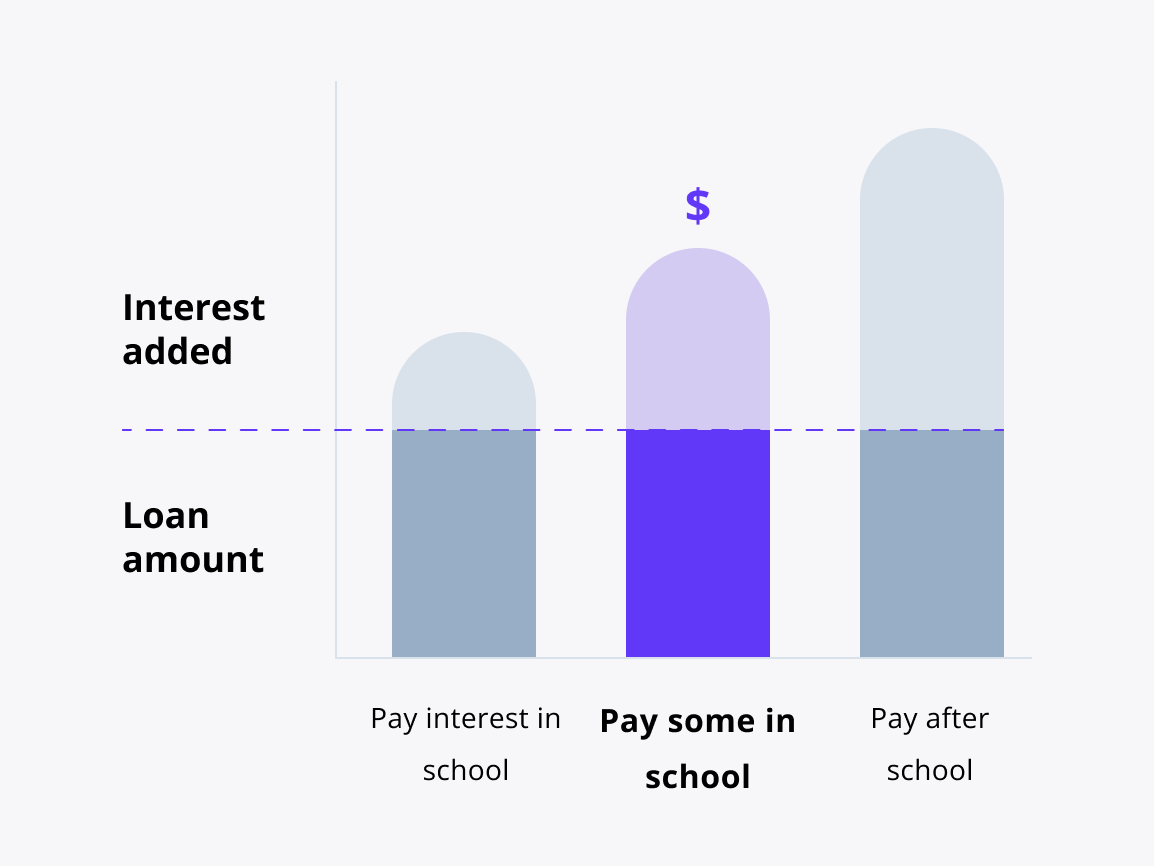

Fixed repayment option

How does it work?

A payment of $25 every monthfootnote 7 is required while your student is in school and in grace.footnote 1

This is a great option if you want to make a dent in payments from the start.

Freshman students may save 7% on their total loan cost by choosing fixed repayment instead of deferred repayment.footnote 6

Keep in mind:

Any interest you don't pay during school will be added to the principal amount (total borrowed) after grace.

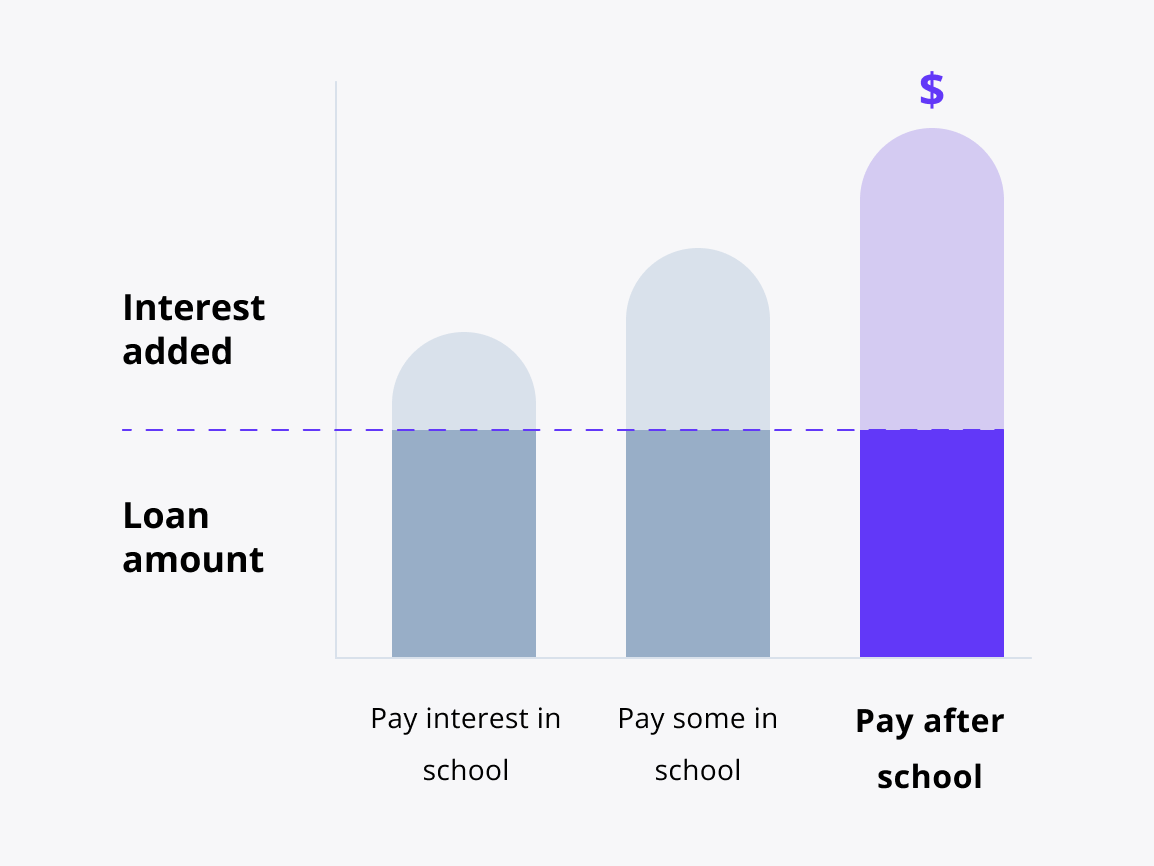

Deferred repayment option

How does it work?

You and your student have no scheduled payments during school and in grace.footnote 1

This is a great option if you and your student want more payment flexibility while your student is in school.

Keep in mind:

The total cost of your loan may be higher because the interest you don’t pay on their loan while they’re in school and grace will be added to the original amount they borrowed (principal amount).

FAQs

Have questions about cosigning? We've got answers.