Together you’ve got this

If you’re a parent (or trusted supporter) exploring student loan options, cosigning is a great way to help your student move forward.

Undergraduate Student Loans:

Fixed rates: 2.09% to 17.49% APRfootnote 1

Variable rates: 3.62% to 16.83% APRfootnote 1

Lowest fixed and variable rates include the autopay interest rate reduction.

If you’re a parent (or trusted supporter) exploring student loan options, cosigning is a great way to help your student move forward.

Undergraduate Student Loans:

Fixed rates: 2.09% to 17.49% APRfootnote 1

Variable rates: 3.62% to 16.83% APRfootnote 1

Lowest fixed and variable rates include the autopay interest rate reduction.

Benefits you won’t want to miss

Cover up to 100% of school-certified expenses, including books, meals, housing, and even a laptop.footnote 2

Undergraduate students were 6.5x more likely to be approved when applying with a cosigner last year.footnote 3

Your student can apply to release their cosigner after meeting requirements.footnote 4

Make payments while your student is in school or defer until after graduation. There’s no upfront fee or penalty for prepayment.footnote 5

You’re there for your student

- Most students don’t have the credit history to take out a private loan on their own, which is why many families look into parent student loans or parent-cosigned options. In fact, 91% of our new Sallie Mae® Undergraduate Student Loans were cosigned last year.footnote 6

- A cosigner can be a parent, or any responsible adult who agrees to share responsibility for the loan. Last year, 27% of Sallie Mae® Undergraduate Student Loan applications were cosigned by an individual other than a parent.footnote 7

- Having a cosigner may also help your student get a lower interest rate.

Breaking down your repayment options

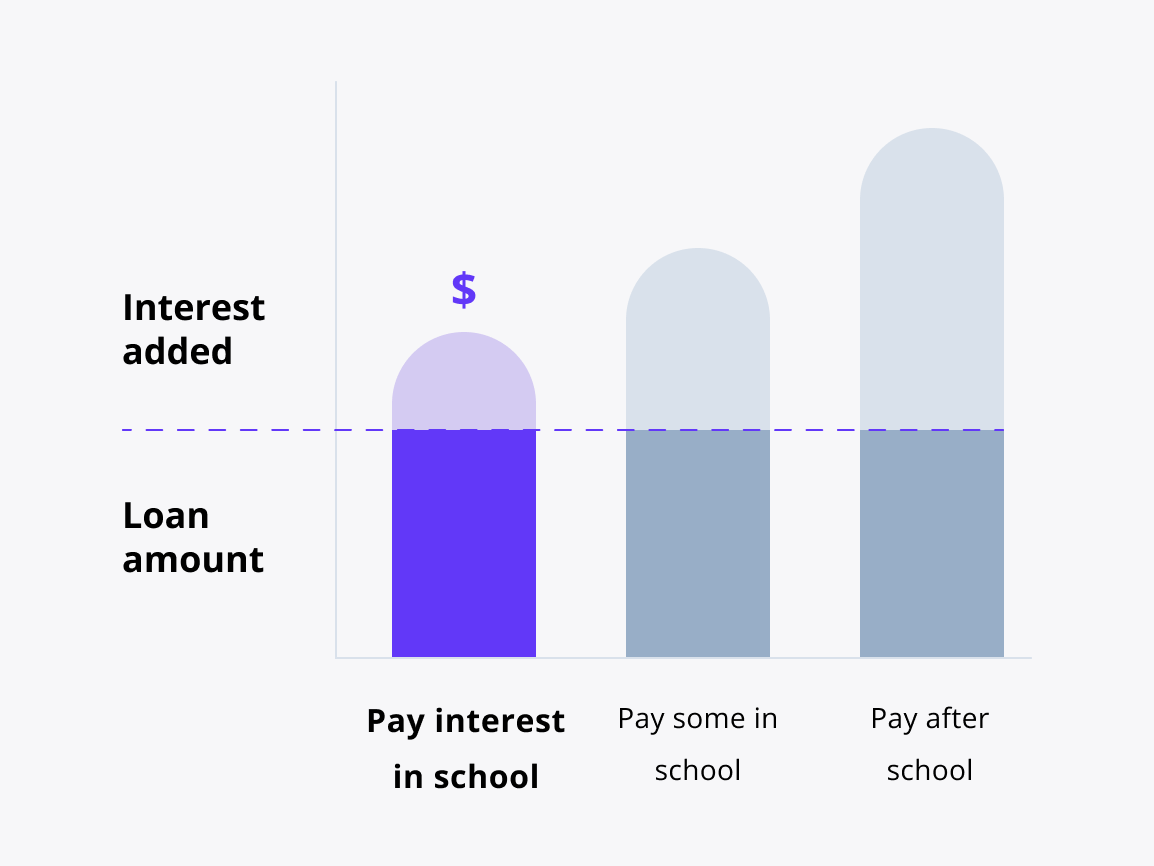

Interest repayment option

How does it work?

Your student pays the monthly interest while they’re in school and during the 6-month grace period to lower the loan cost.footnote 1

This is a great option if your student wants to save the most.

As a freshman, your student may save 17%footnote 8 on the total loan cost if they choose this option instead of paying everything after school.

Keep in mind:

The loan payments will likely be larger while your student is in school and during the grace period than with our fixed or deferred options.

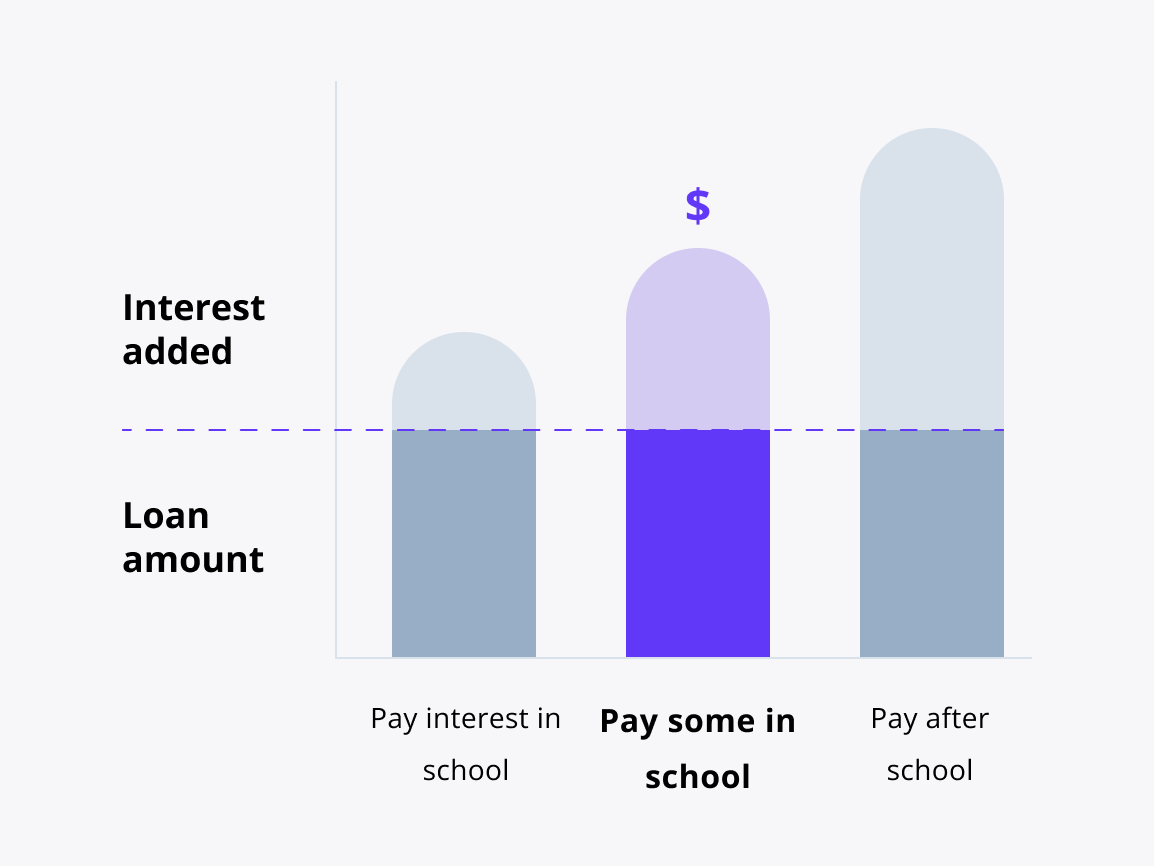

Fixed repayment option

How does it work?

Your student pays $25 a monthfootnote 9 while they’re in school and during the 6-month grace period to lower the loan cost.footnote 1

This is a great option if your student wants to make a dent in payments from the start.

As a freshman, your student may save as much as 7%footnote 8 on their total loan cost if they choose this option instead of paying everything after school.

Keep in mind:

Any interest you don’t pay during school will be added to your principal amount (total borrowed) after grace.

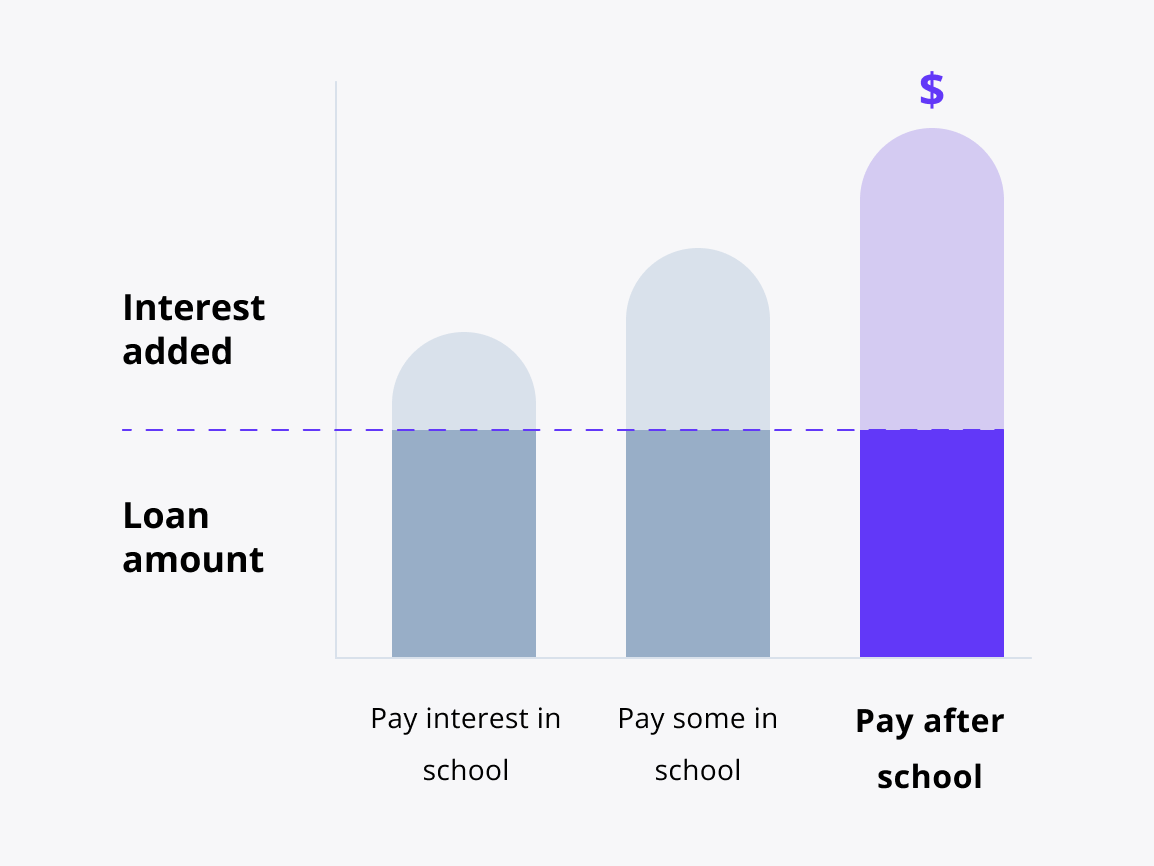

Deferred repayment option

How does it work?

You have no scheduled payments while you’re in school and in grace (the 6 months after leaving school).footnote 1

This is a great option if you want to focus on class and not on making loan payments.

Keep in mind:

The total cost of your loan may be higher because the interest you don’t pay on your loan while you’re in school and grace will be added to the original amount you borrowed (principal amount).

become a

cosigner in

minutes

Follow these steps:

1. Tell us some basics

2. Choose your loan options

3. Sign and accept

FAQs on cosigning undergraduate student loans