If federal loans don’t cover all your college costs, we can help

Over the past 10 years, we’ve paid out more than $8 billion in loans for undergraduate students at interest rates lower than a Parent PLUS loan.

Undergraduate Student Loans:

Fixed rates: 2.09% to 17.49% APRfootnote 1

Variable rates: 3.62% to 16.83% APRfootnote 1

Lowest rates shown/APR shown includes the auto debit discount.

Over the past 10 years, we’ve paid out more than $8 billion in loans for undergraduate students at interest rates lower than a Parent PLUS loan.

Undergraduate Student Loans:

Fixed rates: 2.09% to 17.49% APRfootnote 1

Variable rates: 3.62% to 16.83% APRfootnote 1

Lowest rates shown/APR shown includes the auto debit discount.

Cover up to 100% of school-certified expenses, including books, meals, housing, and even a laptop.footnote 2

There’s no fee to process a loan or if you pay it off early.footnote 3

Pick between competitive fixed or variable interest rates for your college journey.

Your term is based on how much you borrow—so your payments make sense.

Compare loan options to see what works best for your goals

|

Sallie Mae private student loans |

Federal Direct PLUS Loansfootnote 4 |

|

|---|---|---|

|

No upfront fees |

|

|

|

Less than half-time enrollment eligibility |

|

|

|

Fixed and variable interest rate options |

|

|

|

Cover up to 100% of the cost of attendance minus financial aidfootnote 2 |

|

|

|

Rate reduction when you enroll in autopayfootnote 5 |

|

|

|

Credit check required |

|

|

Complete your application in minutes

A Sallie Mae® private student loan can help

If you’ve completed your FAFSA® and explored financial aid or federal loan options and still need additional support, our private student loans can help close the gap when a federal loan doesn’t cover the full cost of college.

Breaking down your repayment options

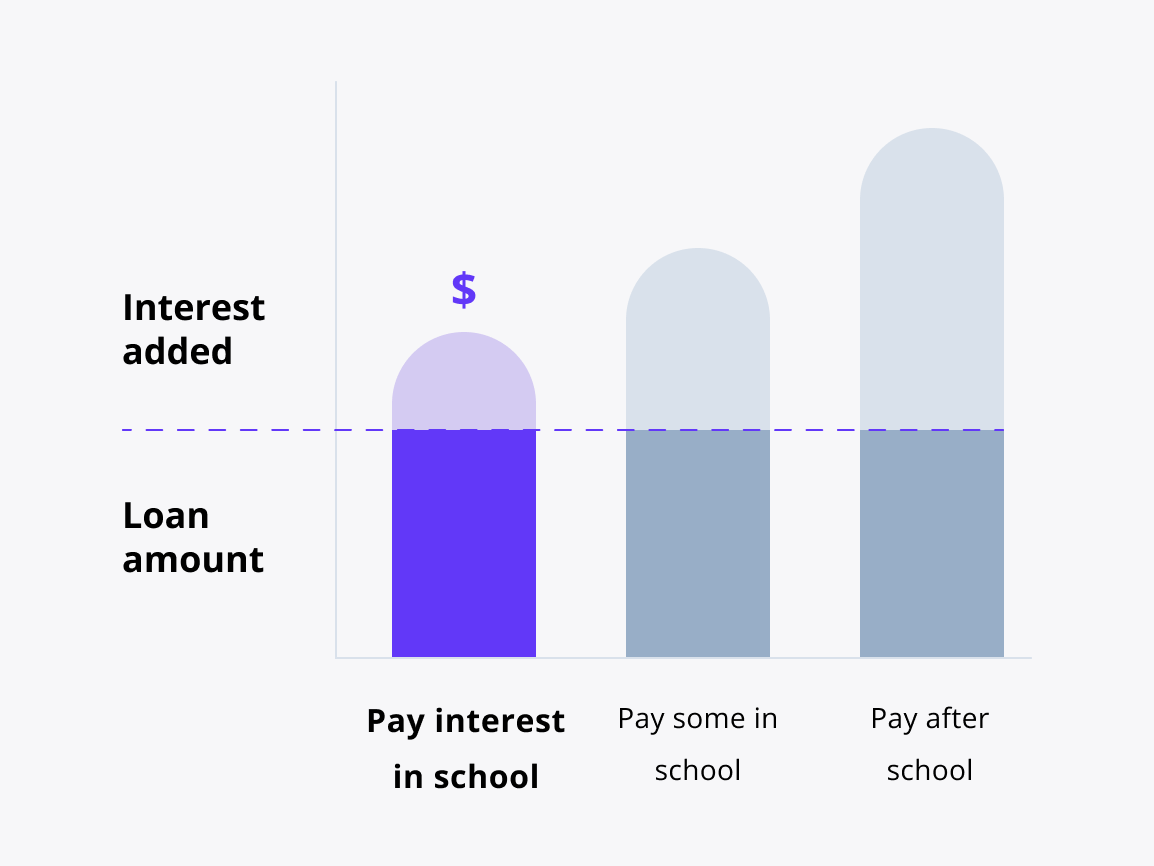

Interest repayment option

How does it work?

You pay your interest every month you’re in school and in grace (the 6 months after leaving school).footnote 1

This is a great option if your student wants to save the most.

Freshman students may save 17% on their total loan cost by choosing interest repayment instead of deferred repayment.footnote 6

Keep in mind:

You might have higher monthly payments during school, but the total cost of your loan may be lower.

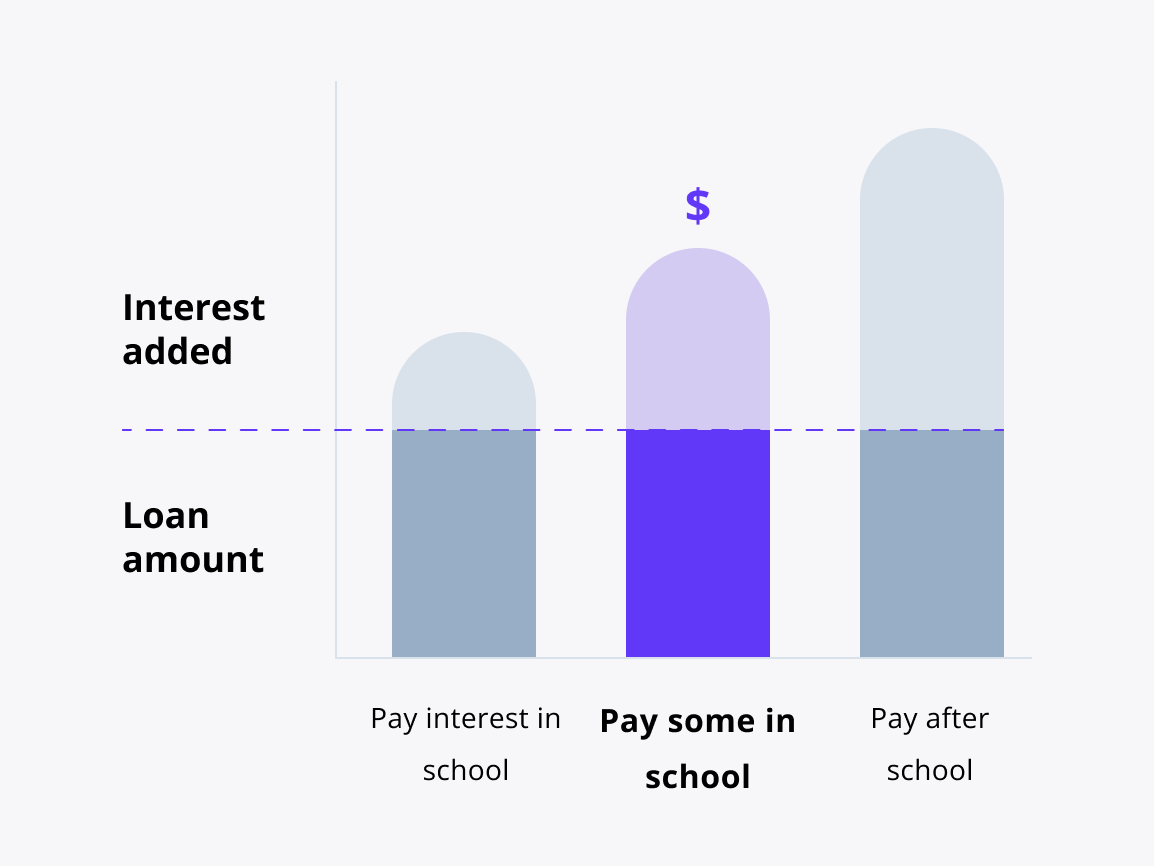

Fixed repayment option

How does it work?

You pay $25 every monthfootnote 7 while you’re in school and in grace (the 6 months after leaving school).footnote 1

This is a great option if your student wants to make a dent in payments from the start.

Freshman students may save 7% on their total loan cost by choosing fixed repayment instead of deferred repayment.footnote 6

Keep in mind:

You might have higher monthly payments during school, but the total cost of your loan may be lower.

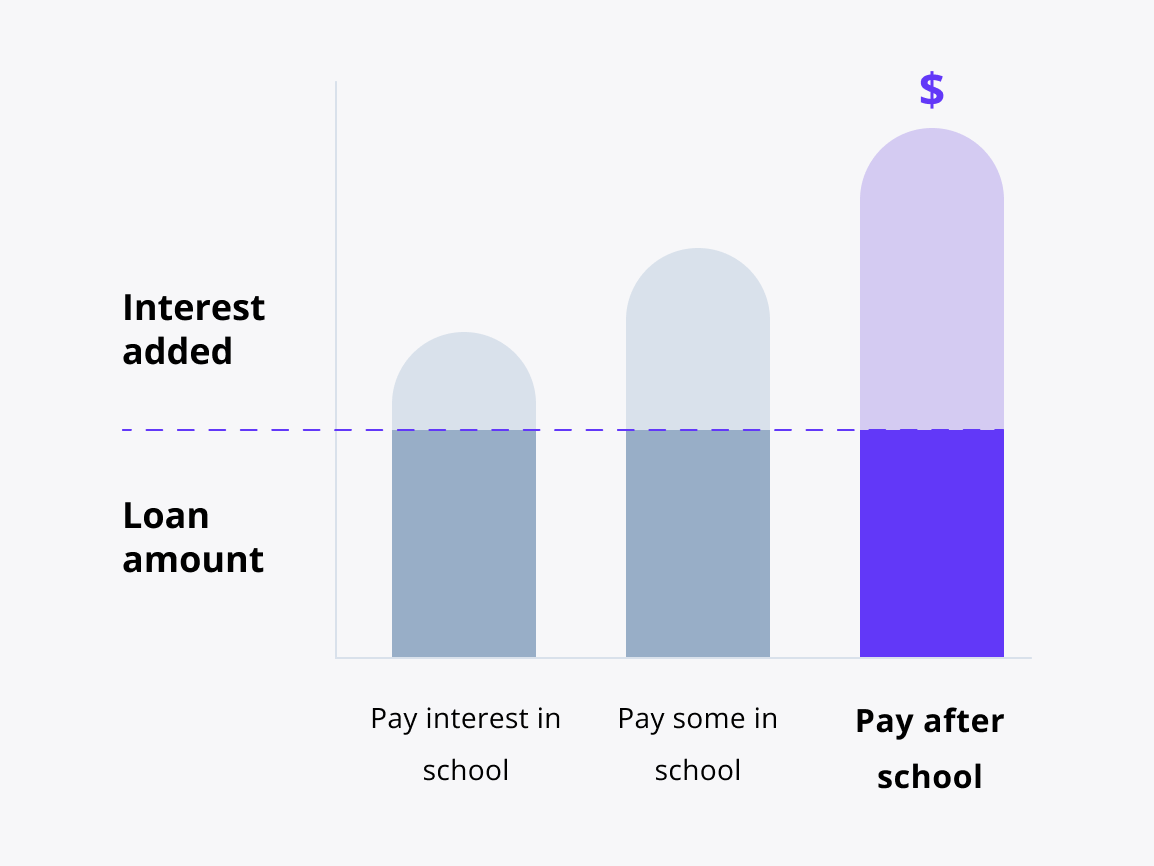

Deferred repayment option

How does it work?

You have no scheduled payments while you’re in school and in grace (the 6 months after leaving school).footnote 1

This is a great option if you want to focus on class and not on making loan payments.

Keep in mind:

The total cost of your loan may be higher because the interest you don’t pay on your loan while you’re in school and grace will be added to the original amount you borrowed (principal amount).

started

Follow these steps:

1. Tell us the basics

2. Customize your loan

3. Sign and accept

Questions?

We're here to help