Your success starts with a medical school loan

Cover medical school and related expenses as you earn your MD, DO, DPM, DVM, or VMD.

2.09%

to 14.97% APRfootnote 1

If you want a predictable monthly payment, this is the way to go.

3.62%

to 14.33% APRfootnote 1

This means your monthly payments may also change—they might be higher if interest rates rise and lower if they fall.

Benefits and support that lasts, from first class to first patient

Medical school is a major commitment, academically and financially. Our medical school loan covers tuition, supplies, and living expenses, so you can concentrate on becoming a doctor, surgeon, dentist, anesthesiologist, pediatrician, veterinarian, or medical researcher—without financial stress.

Up to 100% coverage

of your school-certified costs like tuition, fees, housing, meals, travel, and more.footnote 4

Graduate borrowers were 2x more likely to get approved without a cosigner than undergraduates last year.footnote 5

Make 12 interest-only payments after your grace period.footnote 6

Months of deferment during your residency and fellowship.footnote 7

Month grace period to support your medical career.footnote 8

Breaking down your repayment options

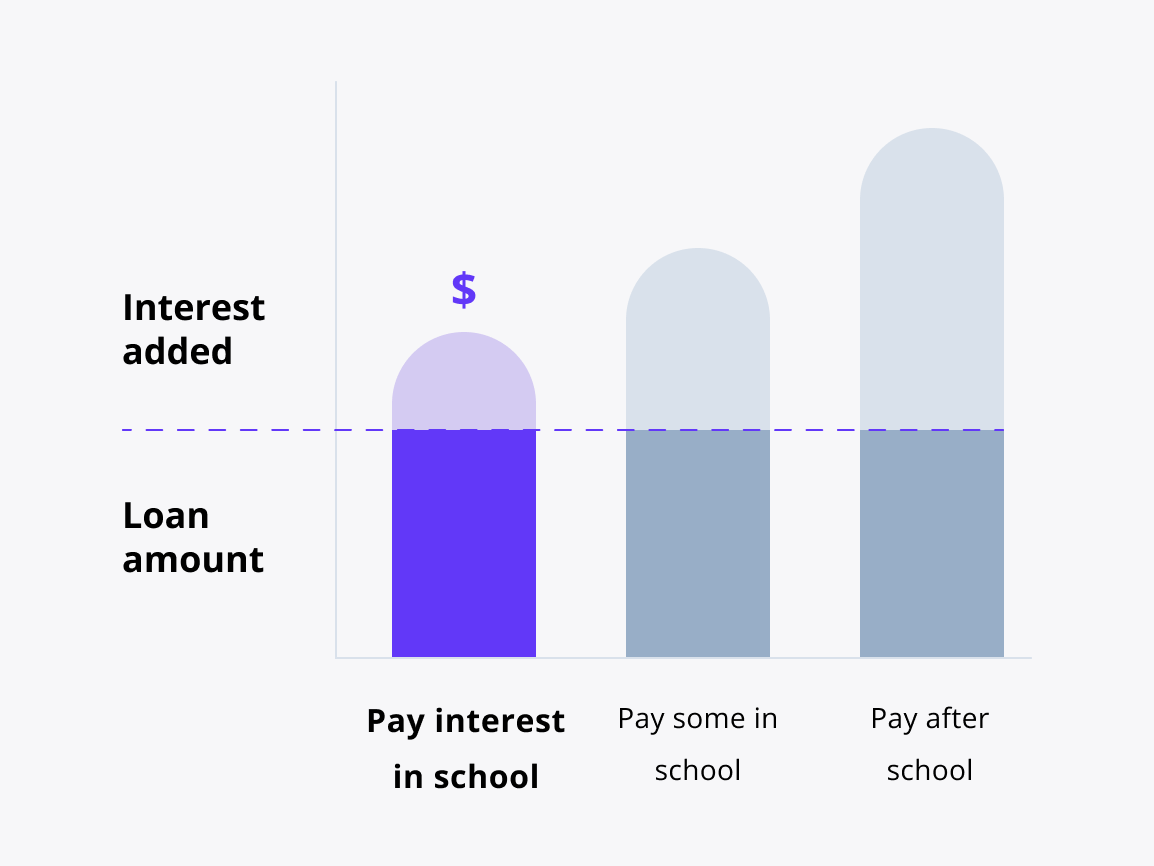

Interest repayment option

How does it work?

You pay your interest every month you’re in school and in grace (the 48 months after).footnote 1

This is a great option if you want to save the most.

Students may get an interest rate that is .50 percentage points lower than deferred repayment.footnote 1

Keep in mind:

You might have higher monthly payments, but the total cost of your loan may be lower.

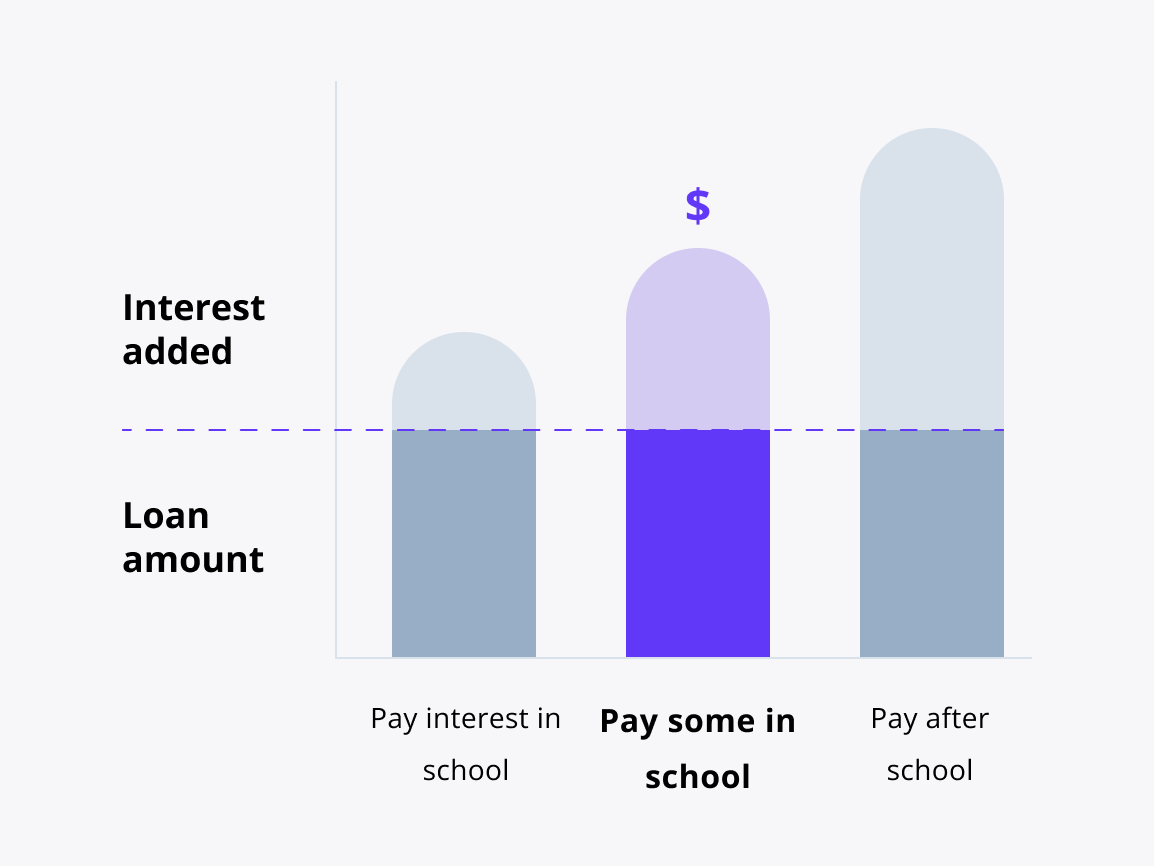

Fixed repayment option

How does it work?

You pay $25 every monthfootnote 9 you’re in school and in grace.footnote 1

This is a great option if you want to make a dent in payments from the start.

Students may get an interest rate that is .25 percentage points lower than deferred repayment.footnote 1

Keep in mind:

Any interest you don’t pay during school will be added to your principal amount (total borrowed) after grace.

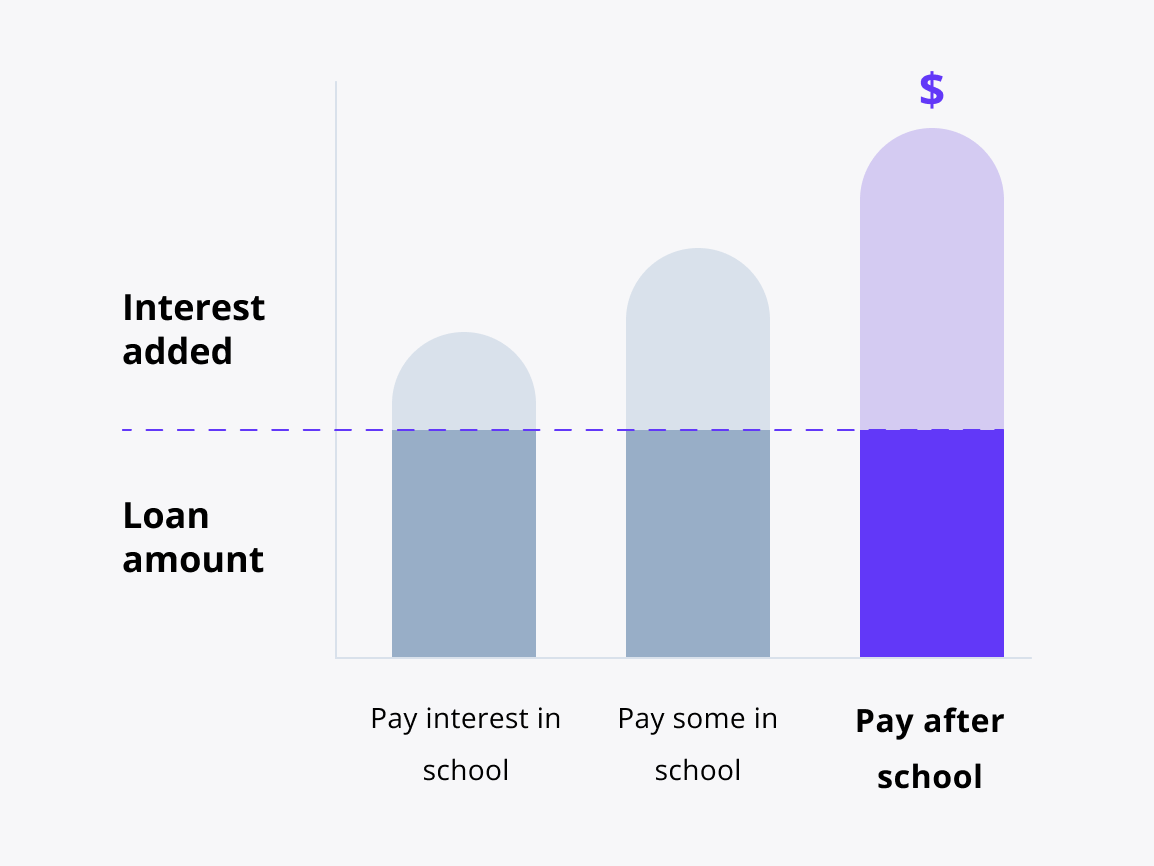

Deferred repayment option

How does it work?

You’ll have no scheduled payments while you’re in school and in grace.footnote 1

This is a great option if you want to focus on class and not on making loan payments.

Keep in mind:

The total cost of your loan may be higher because the interest you don’t pay on your loan while you’re in school and grace will be added to the original amount you borrowed (principal amount).

minutes

1. Tell us some basics

2. Choose your loan options

3. Sign and accept

Doing a medical residency or fellowship?

Our medical residency and relocation loan can help you cover board examination, interview travel, and moving costs.

FAQs

Have other questions? We’re here to help.

833-613-8158