Your legal career made possible with a law school loan

Cover law school and related expenses as you earn your JD or LLM.

3.19%

to 14.99% APRfootnote 1

Fixed means your interest rate never changes.

If you want a predictable monthly payment, this is the way to go.

4.37%

to 13.97% APRfootnote 1

Variable interest rates go up or down as the market changes.

This means your monthly payments may also change—they might be higher if interest rates rise and lower if they fall.

Law school student loan benefits

Up to 100% coverage

of your school-certified costs like tuition, fees, housing, meals, travel, and more.footnote 4

Graduate borrowers were 2x more likely to get approved without a cosigner than undergraduates last year.footnote 5

Make 12 interest-only payments after your grace period.footnote 6

Months of deferment during your residency and fellowship.footnote 7

Month grace period to support you during your law career.footnote 8

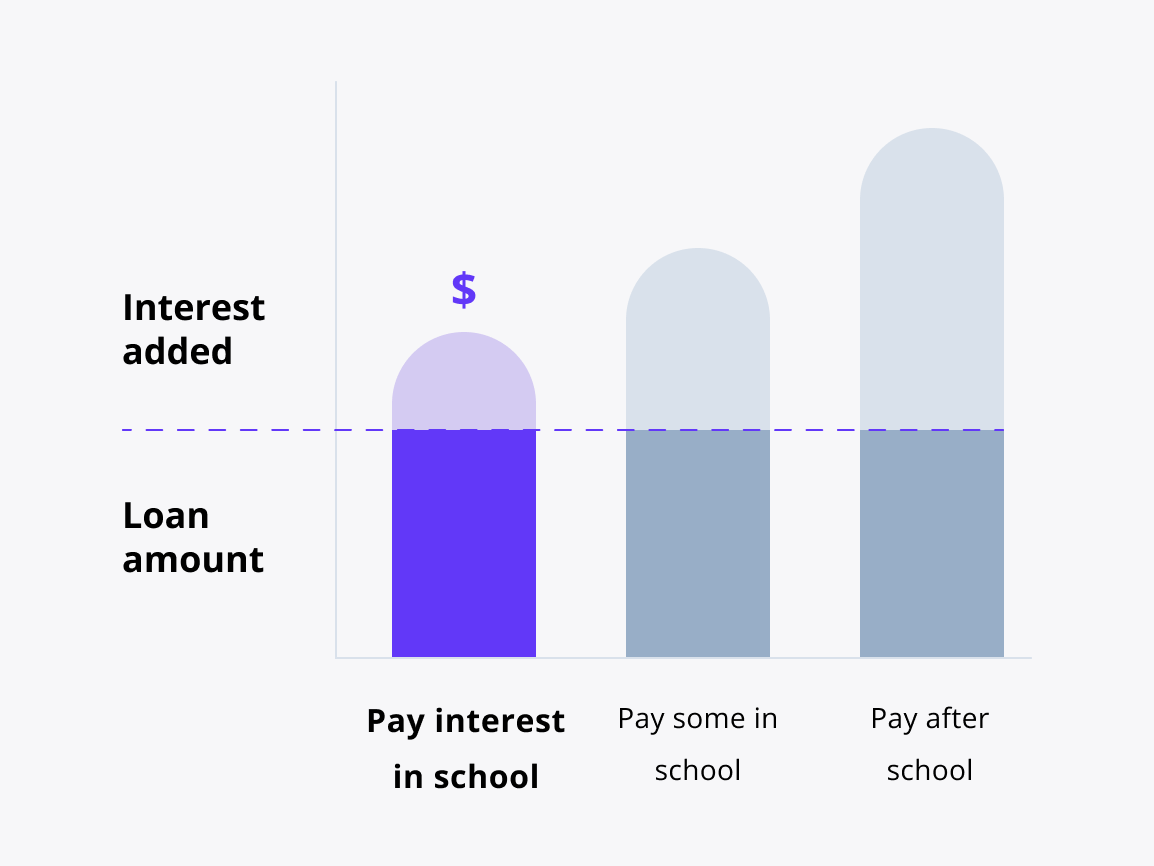

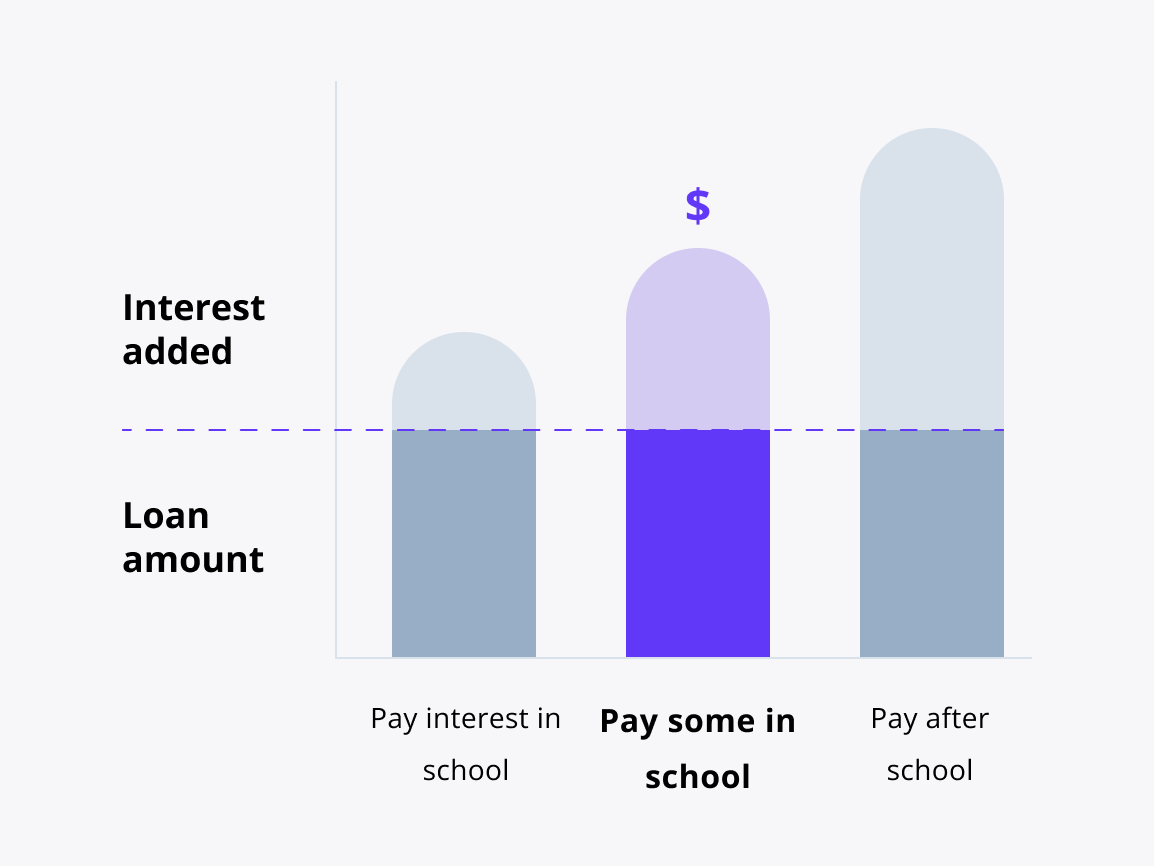

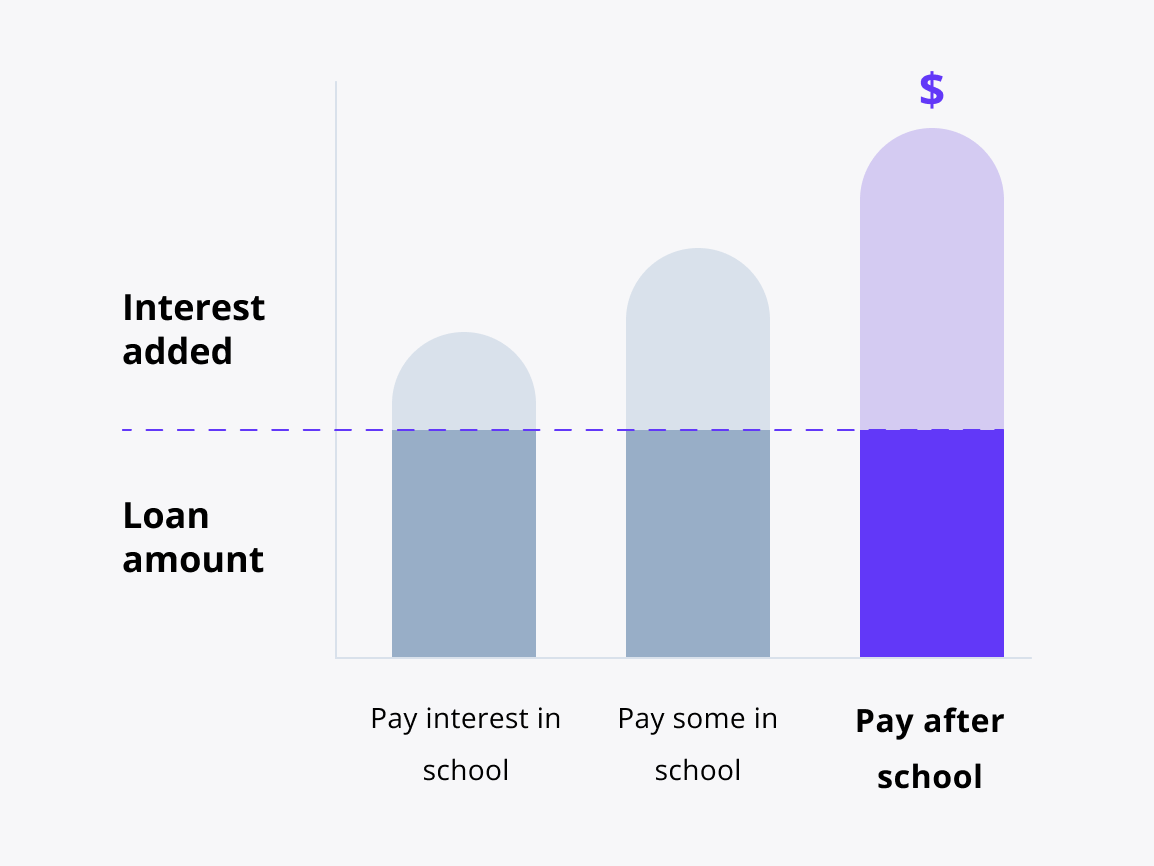

Breaking down your payment options

Interest repayment option

How does it work?

You pay your interest every month you’re in school and in grace (the 9 months after).footnote 1

This is a great option if you want to save the most.

Students may get an interest rate that is .50 percentage points lower than deferred repayment.footnote 1

Keep in mind:

You might have higher monthly payments, but the total cost of your loan may be lower.

Fixed repayment option

How does it work?

You pay $25 every monthfootnote 9 you’re in school and in grace.footnote 1

This is a great option if you want to make a dent in payments from the start.

Students may get an interest rate that is .25 percentage points lower than deferred repayment.footnote 1

Keep in mind:

Any interest you don’t pay during school will be added to your principal amount (total borrowed) after grace.

Deferred repayment option

How does it work?

You’ll have no scheduled payments while you’re in school and in grace.footnote 1

This is a great option if you want to focus on class and not on making loan payments.

Keep in mind:

The total cost of your loan may be higher because the interest you don’t pay on your loan while you’re in school and grace will be added to the original amount you borrowed (principal amount).

What you gain with our law school loan

|

Sallie MaeSM Law School Loan |

Other competitors |

|

|---|---|---|

|

Less than half-time enrollment eligibility |

|

|

|

Apply for cosigner release after 12 months of on-time principal and interest payments and when credit plus other eligibility requirements have been met.footnote 10 |

|

|

|

Interest-only payments for 12 months after grace period for qualifying graduate loan borrowersfootnote 6 |

|

|

|

Multiple repayment terms |

10 to 15-year termsfootnote 9 |

|

|

Cover up to 100% of the cost of attendance minus financial aidfootnote 4 |

|

|

|

Fixed and variable interest rate options |

|

|

|

In-school or deferred repayment options for graduate loan borrowersfootnote 1 |

|

|

minutes

1. Tell us some basics

2. Choose your loan options

3. Sign and accept

Let's make sure you're ready

You’ll need a few things to apply like address, Social Security number (if you have one), and details about your school.

FAQs

Have other questions? We’re here to help.

1-877-279-7172

Are bar exam loans the same as law school loans?

Bar exam loans are not the same as law school loans. Bar exam loans allow law school students nearing graduation to pay for bar study classes, cost of living, the bar exam itself, and other expenses accrued during your time spent studying for the bar. Law school loans help you pay for law school and all law-school related expenses during any year of school.

What does the law school loan cover?

With the Sallie Mae Law School Loan, you can get up to 100% coverage for all of your school-certified expenses. This includes tuition, fees, books, housing, meals, travel, technology, and more.footnote 4 A law school loan does not cover expenses related to the bar exam. A bar exam loan can help cover living expenses and testing fees for the bar exam.

How much can I borrow in law school loans?

The Sallie Mae Law School Loan can cover up to 100% coverage for all of your school-certified expenses. This includes tuition, fees, books, housing, meals, travel, technology, and more.footnote 4

Do law school loans offer deferment or forbearance options during bar exam preparation or clerkship programs?

A deferment may help you postpone or reduce your law school loan payments during your clerkship or fellowship. It's available in increments of 12 months, up to a total of 48 months.footnote 7

Find out about a clerkship or fellowship deferment

Our bar exam loan can help you pay for bar study-related expenses that aren't covered by federal student loan programs, such as bar exam course fees and deposits.

Are there loan options specifically for part-time or evening law school programs?

The Sallie Mae Law School Loan is available to students enrolled full-time, half-time, and less than half-time. Contact your school to see if there are grants, scholarships, or other forms of financial aid for part-time or evening law school programs.

Can I use law school loans to cover the costs of obtaining state bar admissions and licenses?

Obtaining state bar admissions and licenses are expenses that can be covered with bar exam loans rather than law school loans. Bar exam loans allow law school students nearing graduation to pay for bar study classes, cost of living, the bar exam itself, and other expenses accrued during your time spent studying for the bar