It's your future. Let's fund how you get there.

See if you prequalify before applying. You could get a better rate with a Sallie Mae® undergraduate student loan than a federal PLUS loan.footnote 1

2.89%

to 17.49% APRfootnote 2

If you want a predictable monthly payment, this is the way to go.

3.75%

to 16.37% APRfootnote 2

This means your monthly payments may also change—they might be higher if interest rates rise and lower if they fall.

Benefits you won't want to miss

Up to 100% coverage

of school-certified costsfootnote 6—and you only need to apply once to get set for the whole year.

Of undergrad loans were cosigned

last year.footnote 7 A cosigner may be a guardian, relative, or friend.

Getting approved for a Sallie Mae® loan was fairly simple. And took a huge weight off my shoulders when it came to paying for my education.

Breaking down your repayment options

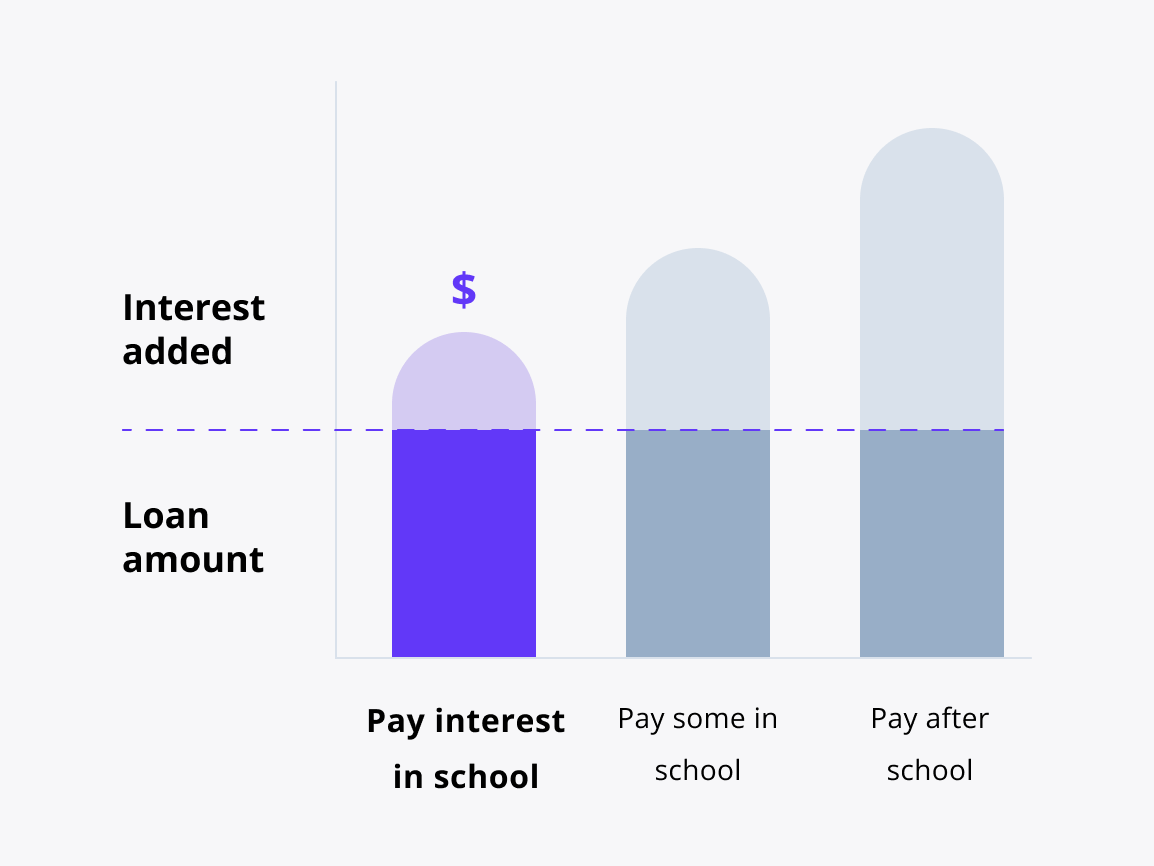

Interest repayment option

How does it work?

You pay your interest every month you’re in school and in grace (the 6 months after).footnote 2

This is a great option if you want to save the most.

Freshman students may save 17% on their total loan cost by choosing interest repayment instead of deferred repayment.footnote 8

Keep in mind:

You might have higher monthly payments, but the total cost of your loan may be lower.

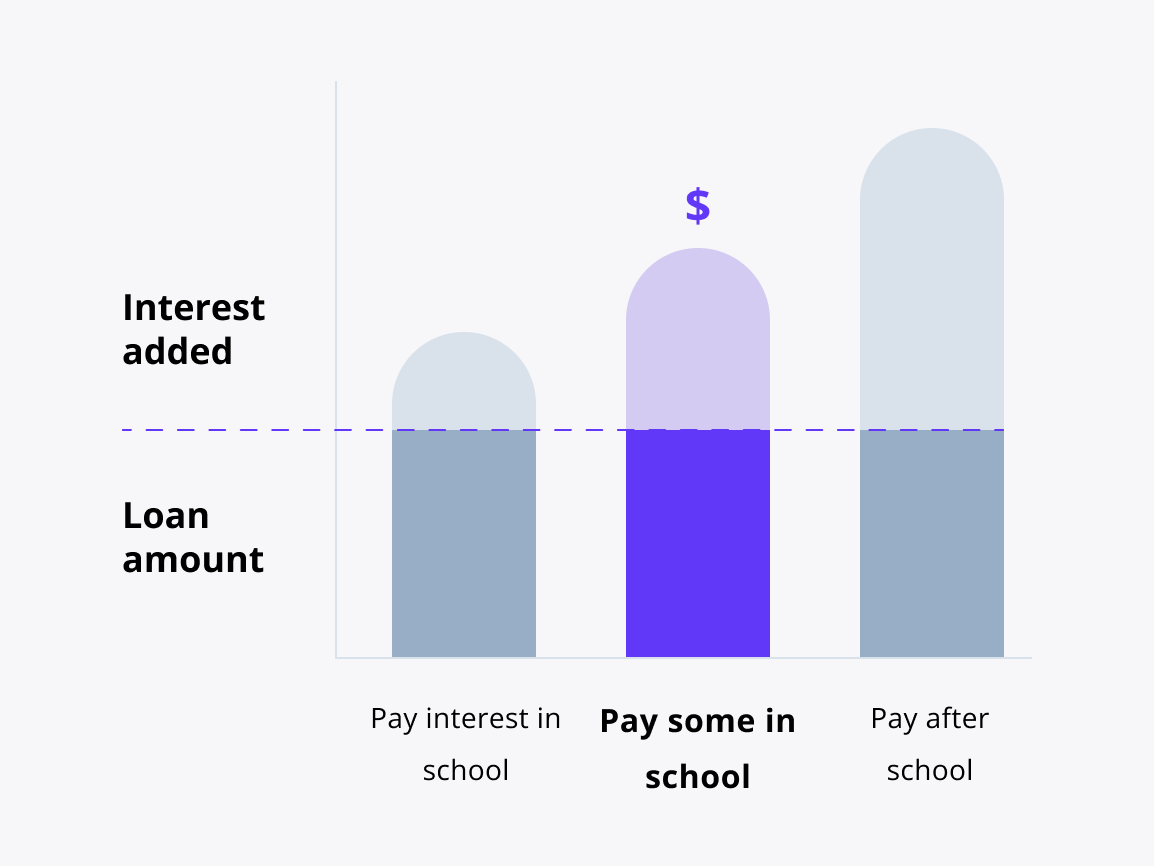

Fixed repayment option

How does it work?

You pay $25 every monthfootnote 9 you’re in school and in grace.footnote 2

This is a great option if you want to make a dent in payments from the start.

Freshman students may save 7% on their total loan cost by choosing fixed repayment instead of deferred repayment.footnote 8

Keep in mind:

Any interest you don't pay during school will be added to your principal amount (total borrowed) after grace.

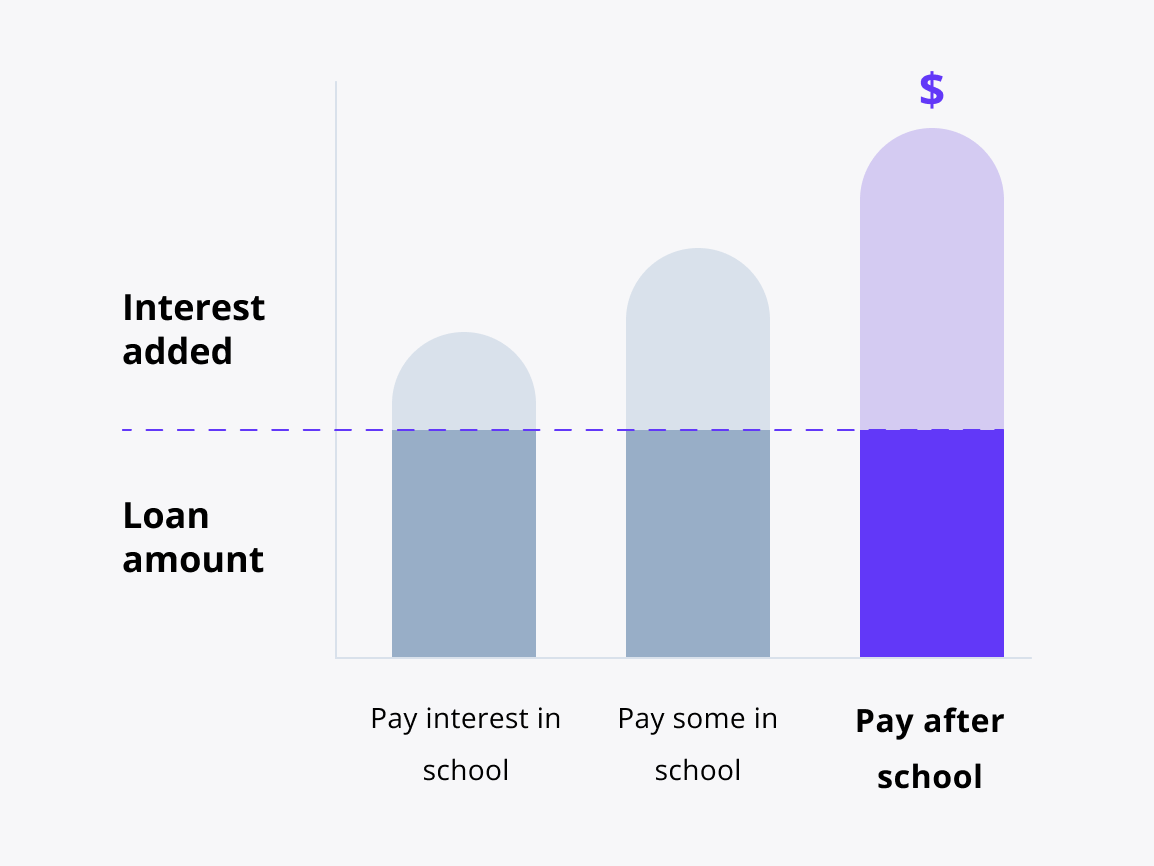

Deferred repayment option

How does it work?

You have no scheduled payments while you’re in school and in grace.footnote 2

This is a great option if you want to focus on class and not on making loan payments.

Keep in mind:

The total cost of your loan may be higher because the interest you don’t pay on your loan while you’re in school and grace will be added to the original amount you borrowed (principal amount).

minutes

1. Tell us some basics

2. Choose your loan options

3. Sign and accept

Let’s make sure you’re ready

You’ll need a few things to apply like address, Social Security number (if you have one), and details about your school.

FAQs

Have other questions? We’re here to help.

1-877-279-7172